TOPIC

06

Navigating ESG Adoption in The Communication and Multimedia Industry: Adoption Benchmark, Challenges, and Strategies by Registered Licensees Under MCMC

LEAD RESEARCHER

Dr. Muhammad Zarunnaim Haji Wahab

UNIVERSITI TEKNOLOGI MARA

TEAM MEMBERS

Mr. Azim Izzuddin Muhamad

UNIVERSITI TEKNOLOGI MARA

Dr. Mohamad Hanif Abu Hassan

UNIVERSITI UTARA MALAYSIA

Dr. Wahidah Shari

UNIVERSITI UTARA MALAYSIA

Abstract

This study examines the adoption of Environmental, Social, and Governance (ESG) principles among Small and Medium Enterprises (SMEs) in Malaysia's Communications and Multimedia (C&M) industry. As global sustainability standards evolve, SMEs face challenges in ESG integration due to financial constraints, limited expertise, and the absence of regulatory mandates. This research aims to identify key barriers, industry-specific considerations, and strategic priorities for effective ESG adoption. A mixed-methods approach was employed, combining surveys and Focus Group Discussions (FGDs) to capture quantitative data and qualitative insights from SME management representatives. Findings reveal that governance is the most prioritised ESG pillar, largely due to regulatory compliance requirements, while environmental initiatives receive the least attention due to high implementation costs. Larger companies with international exposure exhibit structured ESG practices aligned with global standards, whereas SMEs struggle with fragmented and ad-hoc approaches. Key recommendations include the development of simplified ESG guidelines tailored for SMEs, financial incentives such as tax breaks and grants, industry-specific frameworks, and capacity-building initiatives to enhance awareness and implementation. Additionally, stakeholder engagement and phased regulatory enforcement are crucial for fostering a supportive ecosystem for ESG adoption. This study highlights the urgent need for structured ESG support mechanisms to enable SMEs to contribute effectively to Malaysia's sustainability goals while remaining competitive in an evolving business landscape.

Keywords: ESG adoption, Small and Medium Enterprises, Sustainability practices, Malaysia Communications and Multimedia industry

Introduction

In recent years, growing awareness of Environmental, Social, and Governance (ESG) issues has driven increased attention from stakeholders, including asset owners, investors, and organisations worldwide. Concerns such as climate change, pollution, social inequality, and corporate ethics have highlighted the need for sustainable practices (Boffo & Patalano, 2020). Global frameworks like the Global Reporting Initiative and the United Nations Global Compact have encouraged organisations to integrate ESG principles into their strategies, aligning with the Sustainable Development Goals (SDGs) (Nemoto & Peter, 2020).

ESG integration has become a critical tool for enhancing transparency, accountability, and ethical governance across industries. By embedding ESG considerations into decision-making, organisations can mitigate risks, identify new opportunities, and enhance their reputation (PRI Report, 2019). However, despite its recognised benefits, many companies, particularly Small and Medium Enterprises (SMEs) and non-publicly listed firms, remain unaware of the advantages of ESG adoption. This challenge is particularly evident in the Communications and Multimedia (C&M) industry, where some businesses perceive ESG as non-essential, risking unpreparedness for evolving regulatory and market expectations.

This study examines ESG adoption among C&M industry players by analysing their ESG Ratings and Disclosure Scores. It aims to identify key ESG priorities, assess their impact on organisational success, and explore the risks and challenges of ESG implementation. Research indicates a positive correlation between ESG disclosures and financial performance in Malaysian companies, with higher ESG scores linked to better returns and investment attraction (Mohd Taib & Haron, 2024). Malaysia is also positioning itself as a hub for ESG investments, reinforcing its commitment to sustainability through regulatory support and market-driven initiatives.

The study builds on stakeholder and decision-making theories to understand the factors influencing ESG adoption. Previous research has shown that pressure from stakeholders, corporate governance, and institutional demands play a crucial role in shaping sustainability practices (Astrid & Siregar, 2018; Park & Jae, 2021). By integrating these theoretical perspectives, as shown in Figure 1, this research seeks to bridge gaps in ESG adoption, particularly among SMEs in the C&M industry, and propose strategies for overcoming implementation barriers. The findings will contribute to advancing ESG practices, fostering sustainable development, and enhancing corporate resilience in Malaysia.

Stakeholder Theory

Emphasises the interconnected relationships between a business and its customers, suppliers, employees, investors, communities and others who have an interest in the organisation

Decision Theory

To make the best choices under uncertainty and risk

Level of

ESG Adoption

Figure 1: The relationship between stakeholder theory and decision theory in influencing the level of ESG adoption.

Problem Statement

Despite the growing global emphasis on ESG principles, ESG adoption in Malaysian companies remains in its early stages. As a key factor in responsible decision-making and long-term value creation, ESG is increasingly recognised as essential for organisational sustainability across various industries. Consequently, investors are placing greater importance on ESG considerations when making investment decisions.

In December 2023, Bursa Malaysia launched its ESG Reporting Platform for publicly listed companies on the Main Market and ACE Market. However, these regulatory measures apply only to publicly listed entities, leaving non-publicly listed companies and small businesses outside the compliance framework. While businesses are becoming more aware of the tangible benefits of ESG adoption—including enhanced reputation, stronger stakeholder trust, and alignment with consumer expectations—there remains a pressing need for SMEs to integrate ESG principles into their operations.

This research aims to deepen the understanding of ESG adoption within the C&M industry by analysing comparative ESG Ratings and ESG Disclosure Scores. The study will evaluate key areas of ESG implementation, assess the significance of various ESG investments, and identify challenges and risks associated with ESG adoption. Additionally, it seeks to provide practical insights and strategic recommendations to support businesses, particularly SMEs, in navigating their ESG journey effectively.

Research Objectives

In the broader scope, this research aims to investigate the level of ESG adoption among companies in the C&M industry, focusing on SME businesses, as well as to identify the key challenges and risks associated with ESG adoption and strategies for overcoming them. The specific objectives were as follows:

To identify the key challenges/risks in the ESG and mitigation approaches.

To understand how licensees allocate spending across the three ESG pillars and allocation rationale.

To analyse Licensees' ESG Ratings against ESG Disclosure Scores and propose different measurement indices for each ESG pillar.

Literature Review

Stakeholder theory suggests that businesses should consider both short-term financial goals and broader ESG principles (Wang et al., 2020). Stakeholder pressure—whether from governments, NGOs, the public, shareholders, or employees—plays a key role in corporate decision-making and disaster management (Damert & Baumgartner, 2017). Henriques and Sadorsky (1996) found that pressure from customers, regulators, and community groups encourages environmental initiatives. Similarly, Lee et al. (2018) highlighted that both internal and external stakeholder support drive ESG adoption, enhancing corporate legitimacy and sustainability. Cañón-de-Francia and Garcés-Ayerbe (2019) further demonstrated that environmental focus can provide economic benefits.

Decision-making within organisations is often goal-oriented, with stakeholders’ objectives shaping both strategic choices and overall company performance (Chkanikova & Mont, 2015). Traditional economic theories suggest that decisions are driven by knowledge, experience, expectations, and the ability to capitalise on opportunities (Testa, Boiral, & Iraldo, 2018). Several studies highlight the relationship between environmental considerations and corporate decision-making. For instance, Dowell and Muthulingam (2017) found that investors in the United States consider environmental concerns when assessing a company’s social responsibility. Similarly, Narayanan, Baird, and Tay (2021) revealed that environmental concerns significantly influence Australian managers when setting non-economic investment objectives. In Indonesia, Musfialdy (2019) examined mining companies listed on the Indonesia Stock Exchange from 2013 to 2016 and found that nine companies actively incorporated environmental considerations into their investment decisions

Overall, the literature suggests that integrating ESG principles into decision-making aligns with stakeholder expectations and contributes to long-term sustainability and economic benefits. As companies face increasing environmental and social challenges, embedding ESG considerations in corporate strategies is crucial for resilience and maintaining a competitive edge

Challenges and Risks in ESG Implementation

Based on the literature review, the key challenges and risks associated with ESG implementation can be categorised into internal and external factors.

Internal Factors

Several internal barriers hinder effective ESG integration, including:

- Lack of Awareness: Many employees and management personnel are unaware of ESG principles and their significance, slowing down adoption efforts (Jegatheswaran Ratnasingam et al., 2023). Studies indicate that companies with comprehensive ESG awareness programmes demonstrate higher implementation success rates.

- Organisational Culture: Resistance to change within company culture can obstruct ESG integration, as it often requires a shift in values and priorities (Wu & Tham, 2023). Companies with strong sustainability-oriented cultures often show better ESG performance (Benn et al., 2022).

- Employee Engagement: Companies struggle to engage employees effectively in ESG initiatives, impacting implementation success (Liou et al., 2023). Employee-driven sustainability programmes have been identified as a key success factor in several case studies (Roberts & Green, 2023).

- Management Support: The absence of top management commitment can hinder ESG adoption, as leadership buy-in is critical for resource allocation and strategic planning (Zhang & Zhang, 2023). Organisations with dedicated ESG leadership teams often see more effective implementation (Jackson & Varela, 2024).

- Knowledge and Expertise: A lack of expertise in ESG frameworks among employees prevents organisations from effectively executing sustainability strategies (Dmuchowski et al., 2023). Educational initiatives and partnerships with ESG consultancy firms have proven to be effective solutions (Martin & Lewis, 2023).

- Facilities and Infrastructure: ESG initiatives require proper facilities and infrastructure, particularly for environmental and social governance improvements (Ang et al., 2023). Green infrastructure investments have been linked to better long-term financial performance (Morris & Hartley, 2023).

- Corporate Reputation: Companies fear reputational risks if their ESG initiatives are perceived as insufficient or insincere (Rangel et al., 2024). Transparent ESG reporting and stakeholder engagement strategies help mitigate these risks (West & Patel, 2023).

External Factors

From an external perspective, the following factors affect ESG integration:

- Competitive Pressures: Organisations may hesitate to invest in ESG if competitors do not, fearing a competitive disadvantage (Vivoda & Matthews, 2023). However, studies suggest that first movers in ESG often gain a reputational advantage and long-term financial benefits (Schmidt & Brown, 2023).

- Supplier Practices: ESG integration is contingent on suppliers' sustainability practices, posing a challenge in enforcing compliance across supply chains (Dai & Tang, 2022). Collaborative supplier sustainability programmes have been effective in improving ESG adoption (Lang & Foster, 2023).

- Customer Expectations and Support: Aligning ESG goals with customer preferences is challenging, especially when consumers prioritise cost over sustainability (Fatemi et al., 2018). Research suggests that consumer education and marketing strategies emphasising sustainability benefits can increase ESG product adoption (Williams & Shaw, 2023).

- Government Regulations and Policy Uncertainty: Inconsistent regulatory frameworks and shifting policies create obstacles for companies implementing ESG strategies (Wang, 2024; Rangel et al., 2024). Case studies highlight that firms proactively adapting to emerging ESG regulations tend to have a competitive advantage (Nelson & Cooper, 2023).

- Societal Expectations: Adapting business practices to societal demands for corporate responsibility is complex and requires strategic alignment (Agosto et al., 2023). Companies that actively engage with stakeholders and demonstrate genuine commitment to ESG principles tend to build stronger brand loyalty and social capital.

The literature underscores the importance of ESG integration for corporate sustainability and long-term profitability. Stakeholder pressure, both internal and external, plays a significant role in driving ESG adoption. However, companies face numerous challenges, including organisational resistance, knowledge gaps, regulatory uncertainties, and competitive pressures. Addressing these barriers requires a strategic approach that incorporates awareness-building, leadership commitment, infrastructure investment, and regulatory compliance. As ESG considerations become increasingly critical in the global business landscape, organisations that proactively integrate sustainability into their decision-making processes will be better positioned to thrive in a competitive and socially responsible market.

Methodology

In order to achieve the objectives progressively, mixed method research adopted by using questionnaires survey and Focus Group Discussions (FGDs). Details, as follows:

Research DESIGN

A total of 330 SMEs were randomly selected from the MCMC database to ensure diverse representation across company sizes and locations. A structured questionnaire with 116 questions was developed to assess ESG practices, covering environmental strategies, social engagement, and governance structures. The questionnaire was divided into three sections: identifying key ESG adoption challenges and mitigation strategies, analysing resource allocation across ESG pillars, and examining the correlation between ESG Ratings and ESG Disclosure Scores using specific metrics like carbon footprint and transparency. A pilot study was conducted to refine the questionnaire for clarity and relevance. Data collection was carried out online and through physical distribution, with an estimated response time of 10 to 15 minutes. To improve response rates, one research assistant and three enumerators facilitated survey distribution and follow-ups.

SAMPLING

The target population for this study consisted of management-level individuals from SMEs within the C&M industry. The intended sample size for the questionnaire survey was 330 respondents; however, only 61 valid responses were received and included in the analysis.

For the Focus Group Discussion (FGD), participants comprised representatives from C&M companies, the MCMC, and other relevant sectors. A total of up to nine informants actively participated in the FGD sessions, contributing valuable insights to the study.

To ensure the sample's representativeness, random sampling techniques were employed, aiming to select participants from diverse backgrounds and organisational settings. Stratification of the sample based on factors such as age, gender, academic discipline, and job role was implemented to ensure adequate representation across various demographic and professional characteristics. This stratified approach enhanced the study's validity by capturing a wide range of perspectives and experiences within the target population.

DATA COLLECTION

This research employed a mixed-mode methodology, combining qualitative and quantitative approaches, to align with the research objectives and ensure comprehensive data collection. This approach allowed the study to leverage the strengths of both methods, providing a balanced perspective and richer insights into the research topic.

Quantitative Approach: Survey Questionnaires

For the quantitative component, structured survey questionnaires with closed-ended Likert scale questions were used to address research objectives 1 through 3, enabling the measurement of behaviours, attitudes, and demographic characteristics for statistical analysis. To ensure a higher response rate and data reliability, the survey was distributed online and by email, targeting identified respondents. Follow-up phone calls were conducted to encourage participation and address non-responses. This multi-channel approach enhanced coverage and improved the validity of the collected data.

Qualitative Approach: Focus Group Discussions (FGDs)

For the qualitative component, FGDs were conducted to address research objective 4, providing a platform for guided discussions that captured diverse perspectives, experiences, and attitudes. Semi-structured questions ensured a focused yet flexible dialogue, allowing participants to introduce new insights beyond the scope of quantitative surveys. To ensure a broad representation of stakeholder views, participants were carefully selected from various groups, and an experienced facilitator moderated each session to encourage equal participation. Discussions were recorded and transcribed for thematic analysis, preserving the depth and integrity of the collected data.

DATA ANALYSIS

The analysis of the questionnaire survey employed statistical techniques such as descriptive statistics, regression analysis, or other related methods using SPSS to identify patterns and relationships. The outcomes from the questionnaires were used to develop a draft ESG adoption guide for industries, which was subsequently refined through FGD sessions to incorporate additional input and verification from experts. The analysis of FGDs involved systematically organising, coding, and interpreting the collected data to uncover patterns, themes, and insights relevant to the research questions. The process consisted of several key steps: transcription, coding, categorisation, data reduction, interpretation, triangulation, and report writing.

Findings and Analysis

The discussion of findings provides an in-depth analysis of the key insights derived from the study, focusing on the implementation of ESG practices among C&M organisations. This section examines the challenges faced in ESG adoption, the strategic allocation of resources across the ESG pillars, and the frameworks used to measure ESG performance. By integrating descriptive analysis with reliability tests, the discussion explores the varying levels of ESG engagement, particularly between SMEs and larger organisations.

DESCRIPTIVE ANALYSIS

Age of Respondents

Age of Respondents

Figure 2: : Age of Respondents.

Figure 2 illustrate the age distribution of respondents, categorised into four distinct groups: 20 to 30 years, 31 to 40 years, 41 to 50 years, and 51 years and above. Among these, the majority of respondents (37.7 per cent, n=23) fall within the 41–50 years age group, indicating that this category constitutes the largest segment of the sample. The second-largest group consists of respondents aged 51 years and above, accounting for 26.2 per cent (n=16) of the total. This is followed by the 31 to 40 years age group, which comprises 23 per cent (n=14) of the respondents. The smallest proportion of participants is found in the 20 to 30 years age group, representing only 13.1 per cent (n=8) of the sample. Cumulatively, 63.9 per cent of respondents are aged 41 years and above, suggesting a significant concentration of older participants in the sample. This age distribution may have implications for the findings, particularly in relation to any variables that might be influenced by the respondents' age.

Gender

Gender of Respondents

Figure 3: Gender of Respondents.

The gender distribution of the respondents indicates a slightly higher representation of males compared to females as illustrated in Figure 3. Out of the total 61 respondents, 32 individuals (52.5 per cent) are male, while 29 individuals (47.5 per cent) are female. This distribution shows a fairly balanced representation of genders, with a modest predominance of males within the sample.

Type of company registration

Type of company registration

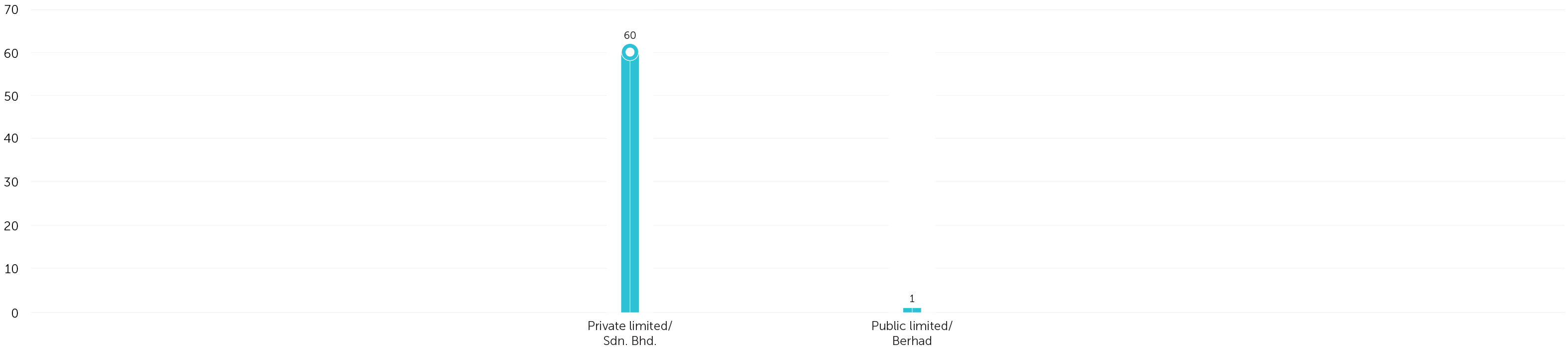

Figure 4: Type of company registration

Figure 4 illustrates the vast majority of respondents, 60 out of 61 (98.4 per cent), represent private limited companies (Sdn. Bhd.), indicating that this is the most common business structure among the sample. Only a small proportion of respondents are affiliated with other types of companies, with 1 respondent (1.7 per cent) representing a public limited company (Berhad).

Does the company have subsidiaries abroad?

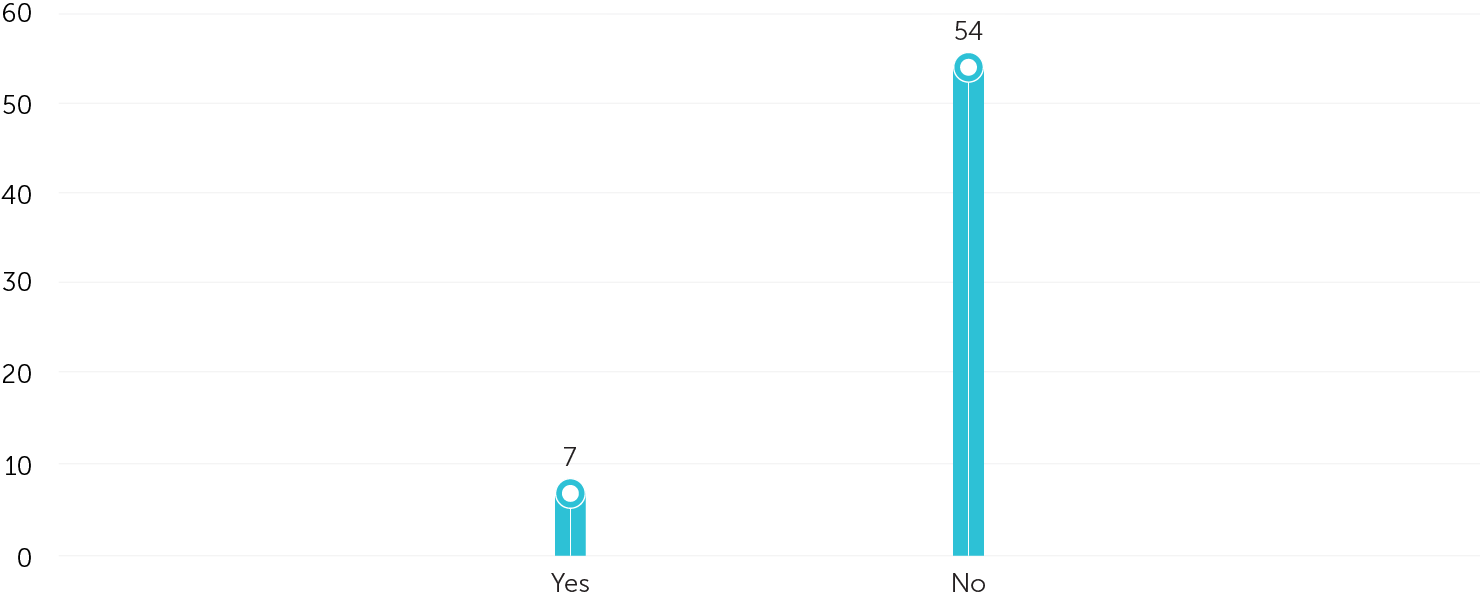

Does the company have subsidiaries abroad?

Figure 5: Does the company have subsidiaries abroad?

Figure 5 illustrates the majority of respondents, 54 out of 61 (88.5 per cent), indicated that their companies do not have subsidiaries abroad. Only a small proportion, 7 respondents (11.5 per cent), reported that their companies do have subsidiaries in foreign locations. This distribution underscores that most companies in the sample are domestically focused, with a minority having international operational extensions

Company revenue for the year 2023

Company revenue for the year 2023

Figure 6: Company revenue for the year 2023.

The data on company revenue for 2023 reveals a diverse range of financial performance among the sampled companies as illustrated in Figure 6. Notably, the largest proportion of companies, 31.1 per cent (n=19), reported annual revenues exceeding RM15,000,000. This indicates a significant presence of high-revenue companies within the sample, suggesting that a substantial portion of the businesses operate at a large scale or within high-revenue industries. On the other hand, a considerable number of companies reported revenues within the mid to lower ranges. For instance, 19.7 per cent (n=12) earned between RM1,000,001 and RM5,000,000, 16.4 per cent (n=10) earned between RM300,001 and RM1,000,000 and 13.1 per cent (n=8) earned between RM5,000,001 to RM10,000,000. Together, these three categories represent a significant portion of mid-sized companies, highlighting the diversity in company sizes within the sample. At the lower end of the revenue spectrum, 9.8 per cent (n=6) of companies reported earning less than RM300,000 annually, reflecting a smaller subset of businesses that may be in the early stages of operation or engaged in low-revenue sectors. Similarly, 9.8 per cent (n=6) of companies fell into the RM10,000,001 to RM15,000,000 range, showcasing a smaller group of well-established but not top-tier revenue-generating companies. Cumulatively, 45.9 per cent of companies earned revenues of RM5,000,000 or less, while the remaining 54.1 per cent exceeded this amount. This distribution suggests that while the sample includes a notable number of high-performing companies, there is also a strong representation of mid-sized and smaller enterprises.

Number of employees

Number of employees

Figure 7: Number of employees.

The data on the number of employees within the sampled companies reveals a varied distribution as illustrated in Figure 7, reflecting a mix of small, medium, and larger organisations. The majority of companies, 45.9 per cent (n=28), reported having between 6 to 35 employees, indicating that a significant portion of the sample consists of small to medium-sized enterprises (SMEs). This category dominates the sample, highlighting its importance in the overall business landscape represented. A notable proportion, 18.0 per cent (n=11), are micro-enterprises with 1 to 5 employees, reflecting businesses operating on a smaller scale. These companies may represent startups, family-run businesses, or those in specialised niches. The data also shows representation of companies with 36 to 74 employees (16.4 per cent, n=10) and those with more than 75 employees (19.7 per cent, n=12). These categories reflect medium to larger businesses, with the latter group likely representing more established or resource-intensive operations. Cumulatively, 63.9 per cent of companies reported having 35 or fewer employees, emphasising the predominance of SMEs in the sample. Meanwhile, 36.1 per cent reported having 36 or more employees, signifying a smaller but significant presence of medium to large organisations.

RESEARCH QUESTION 1

This section discusses findings related to the first research question, what are the primary challenges and risks associated with implementing ESG practices? The focus of this analysis is to identify the barriers organisations encounter in adopting ESG principles, with particular attention to the context of SMEs. The discussion explores the unique constraints faced by SMEs, including resource limitations, lack of expertise, and fragmented regulatory environments, which hinder the effective integration of ESG practices into business operations.

Internal and External Factors

SMEs encounter multiple internal and external challenges in adopting ESG practices. Internally, five key factors hinder adoption: awareness, organisational culture, employee engagement, management support, and knowledge/expertise. Externally, SMEs face challenges from competitive pressure, supplier practices, customer expectations, government regulations, and societal expectations. Table 1 outlines these internal and external challenges and their impact on ESG adoption.

| Internal Factors | External Factors | |||||

|---|---|---|---|---|---|---|

| Variables | Mean | Median | Variables | Mean | Median | |

| ENVIRONMENTAL | Awareness | 3.11 | 3.00 | Competitor | 2.73 | 3.00 |

| Culture | 3.41 | 3.33 | Supplier | 3.38 | 3.00 | |

| Employee | 3.09 | 3.00 | Customer | 2.97 | 3.00 | |

| Knowledge | 2.82 | 3.00 | Government | 3.02 | 3.00 | |

| Support | 3.36 | 3.17 | Social Community | 2.96 | 3.00 | |

| SOCIAL | Awareness | 3.58 | 3.50 | Competitor | 2.47 | 2.50 |

| Culture | 4.01 | 4.00 | Supplier | 3.47 | 3.00 | |

| Employee | 4.00 | 4.17 | Customer | 3.39 | 3.25 | |

| Knowledge | 3.71 | 3.83 | Government | 3.22 | 3.00 | |

| Support | 3.72 | 4.00 | Social Community | 2.71 | 3.00 | |

| GOVERNANCE | Awareness | 3.90 | 4.00 | Competitor | 2.51 | 2.67 |

| Culture | 4.28 | 4.50 | Supplier | 3.58 | 3.33 | |

| Employee | 3.26 | 3.00 | Customer | 3.74 | 3.67 | |

| Knowledge | 3.69 | 4.00 | Government | 3.31 | 3.33 | |

| Management Support | 3.79 | 4.00 | Social Community | 3.29 | 3.00 | |

Table 1: Primary challenges in implementing ESG practices (internal and external factors).

In summary, Figure 8 shows the primary challenges (internal and external factors) faced by SMEs in adoption of ESG practices in their business.

Environmental

Internal factors

Culture

External factors

Supplier

Social

Internal factors

Employee

External factors

Customer

Governance

Internal factors

Culture

External factors

Customer

Figure 8: The primary challenges (internal and external factors) faced by SMEs in adoption of ESG practices.

The findings align with insights from the FGD, which highlight that awareness and knowledge of ESG practices among workers and companies are steadily increasing. Companies are gradually adopting sustainability initiatives, such as paperless transactions, cloud-based reporting systems, and digital documentation, which reduce operational costs and improve efficiency. This growing awareness suggests that knowledge and awareness are no longer the primary barriers to ESG adoption for SMEs. Instead, the focus should shift toward overcoming structural and cultural challenges within organisations, securing management buy-in, and fostering a work environment that actively encourages ESG integration. While SMEs are making progress in incorporating ESG principles, more structured policies and incentives will be necessary to ensure comprehensive adoption across all levels of business operations.

RESEARCH QUESTION 2

The findings reveal that ESG spending is largely influenced by operational constraints, stakeholder pressures, and regulatory requirements rather than a clear strategic framework. Organisations, particularly SMEs, adopt a reactive approach, prioritise governance for compliance, workforce-related social initiatives, and only minimal environmental investments due to financial and technical limitations.

Governance as the Dominant ESG Pillar

Governance spending is consistently prioritised, especially among private limited companies (Sdn. Bhd.), as it directly aligns with compliance requirements and operational stability. SMEs focus on basic regulatory adherence, while larger firms integrate governance within global ESG frameworks. FGD insights confirm that governance is typically the first ESG component adopted, followed by social and environmental initiatives.

Social Pillar: Workforce-Centric Approach

Organisations emphasise workforce well-being, diversity, and inclusion, with high internal consistency in measuring employee-related metrics (Cronbach's Alpha = 0.955). However, broader societal initiatives, such as community engagement, remain inconsistently addressed, particularly by SMEs. A structured assessment framework, like Social Impact Measurement (SIM), is needed to enhance the effectiveness of social spending.

Environmental Spending: Limited and Cost-Constrained

SMEs allocate minimal resources to environmental initiatives due to high costs and lack of expertise. Investments are mainly in cost-saving measures like energy efficiency rather than sustainability-driven projects. Larger firms, particularly those in global markets, allocate more towards environmental compliance. The FGD highlights SMEs' financial struggles in adopting proper waste management practices, emphasising the need for skilled personnel and financial support to bridge the ESG adoption gap between SMEs and larger corporations.

Governance

Governance: The Dominant Pillar in ESG Spending

- Governance is the most consistently prioritised ESG pillar.

- Focus is due to its direct link with compliance and operational stability.

- Governance spending targets regulatory requirements like:

- Financial reporting

- Anti-corruption measures

- Policy documentation.

%20--%3e%3csvg%20version='1.1'%20id='Layer_1'%20xmlns='http://www.w3.org/2000/svg'%20xmlns:xlink='http://www.w3.org/1999/xlink'%20x='0px'%20y='0px'%20viewBox='0%200%2019%2019'%20style='enable-background:new%200%200%2019%2019;'%20xml:space='preserve'%3e%3cstyle%20type='text/css'%3e%20.st0{fill:%232DC1D6;}%20.st1{fill:%23FFFFFF;}%20%3c/style%3e%3cg%3e%3cg%3e%3cpath%20class='st0'%20d='M9.5,19C4.3,19,0,14.7,0,9.5S4.3,0,9.5,0S19,4.3,19,9.5S14.7,19,9.5,19'/%3e%3c/g%3e%3cpolygon%20class='st1'%20points='4.9,5.7%205.8,5.3%209.5,12.6%2013.2,5.3%2014.1,5.7%2010,13.7%209,13.7%20'/%3e%3c/g%3e%3c/svg%3e)

Social

Social Pillar: Focus on Workforce-Centric Metrics

Employee well-being, retention, diversity, inclusion, and satisfaction are prioritised for productivity and stakeholder trust.

Environmental

Environmental Spending: Limited and Resource-Constrained

Low Priority: Environmental initiatives receive minimal attention among SMEs.

Barriers: High costs and technical expertise required to adopt.

Larger Companies' Role: Companies with revenues > RM15 million allocate more resources to environmental initiatives, driven by global competitiveness and stakeholder expectations.

SMEs' Challenges: Limited financial and technical capacity

Figure 9: The SMEs allocation of spending towards each ESG pillar.

Rationale Behind ESG Allocation

The rationale guiding ESG spending allocation is shaped by a combination of regulatory requirements, operational priorities, resource availability, and stakeholder expectations. These factors collectively determine the emphasis placed on each ESG pillar and the strategic or reactive nature of resource distribution.

Regulatory Compliance:

Governance spending is heavily influenced by the need to comply with mandatory regulations, ensuring operational continuity and maintaining stakeholder trust. This compliance-driven approach is particularly pronounced among SMEs of mitigating risks and fulfilling legal obligations.

Operational Necessities:

Social spending often addresses immediate operational needs, such as employee retention, satisfaction, and productivity. This workforce-centric focus reflects a practical approach to ESG allocation, where resources are directed toward initiatives that deliver direct organisational benefits. Such spending is critical for ensuring stability in operations, particularly for companies with constrained resources.

Resource Limitations:

Environmental spending is notably constrained by financial and technical barriers, especially for SMEs. The high costs and expertise required for comprehensive environmental initiatives, such as renewable energy adoption or carbon reduction strategies, often deter investment in this pillar. Consequently, companies tend to focus on low-cost, regulatory-compliant measures, such as waste management or energy efficiency, rather than pursuing proactive sustainability projects.

Stakeholder Influence:

Larger companies with international exposure face greater scrutiny from stakeholders, including investors, customers, and regulatory bodies. This pressure drives a more balanced allocation of resources across all ESG pillars, aligning spending with global sustainability standards. In contrast, domestically focused SMEs are less subject to such scrutiny, resulting in a reactive approach to ESG spending that addresses immediate pressures without a cohesive strategic framework.

The findings reveal that while organisations allocate spending across the three ESG pillars, this allocation is often reactive and influenced by operational and contextual factors rather than guided by a cohesive strategic framework. Governance is the most consistently prioritised pillar, reflecting its direct link to compliance and operational stability. Social spending, though significant, is fragmented, focusing primarily on workforce-related metrics. Environmental initiatives receive the least attention, highlighting the need for targeted support to enable organisations, particularly SMEs, to adopt proactive sustainability practices. Addressing these disparities through tailored frameworks, capacity-building initiatives, and financial incentives is essential to fostering more strategic and balanced ESG spending across organisations. As conclusion, Figure 10 illustrates the rationale behind ESG allocation.

Figure 10: The rationale behind ESG allocation.

RESEARCH QUESTIONS 3

This section examines the ESG measurement frameworks used by organisations, revealing significant disparities influenced by company size, resources, and operational focus. With 98.4 per cent of the sample comprising private limited companies (Sdn. Bhd.), the absence of mandatory ESG reporting results in inconsistent assessments.

For the environmental pillar, SMEs rarely adopt global frameworks like GRI or CDP due to financial and technical constraints. Instead, they measure performance through operational metrics such as energy efficiency, waste management compliance, and water conservation. Larger firms earning over RM15 million annually are more likely to align with global standards, highlighting a benchmarking gap for SMEs.

The social pillar is primarily workforce-centric, with key metrics including employee satisfaction, retention rates, and diversity. The high reliability of social factors (Cronbach's Alpha = 0.955) underscores the focus on employee well-being. However, the absence of structured tools like Social Impact Measurement (SIM) or UN SDG alignment limits broader societal impact assessments.

Governance is the most structured ESG pillar, driven by compliance with financial reporting, anti-bribery policies, and transparency standards. SMEs focus on regulatory adherence, while larger firms integrate international frameworks like ISO 37001 and GRI governance indicators. The governance factors scale (Cronbach's Alpha = 0.936) confirms its reliability but highlights the lack of proactive governance strategies among SMEs.

Overall, the lack of standardised ESG reporting frameworks, particularly for SMEs, creates inconsistencies in performance evaluation. Addressing these gaps requires simplified ESG tools, financial incentives, and capacity-building initiatives to enhance ESG measurement, ensuring sustainability and competitiveness in an evolving global economy.

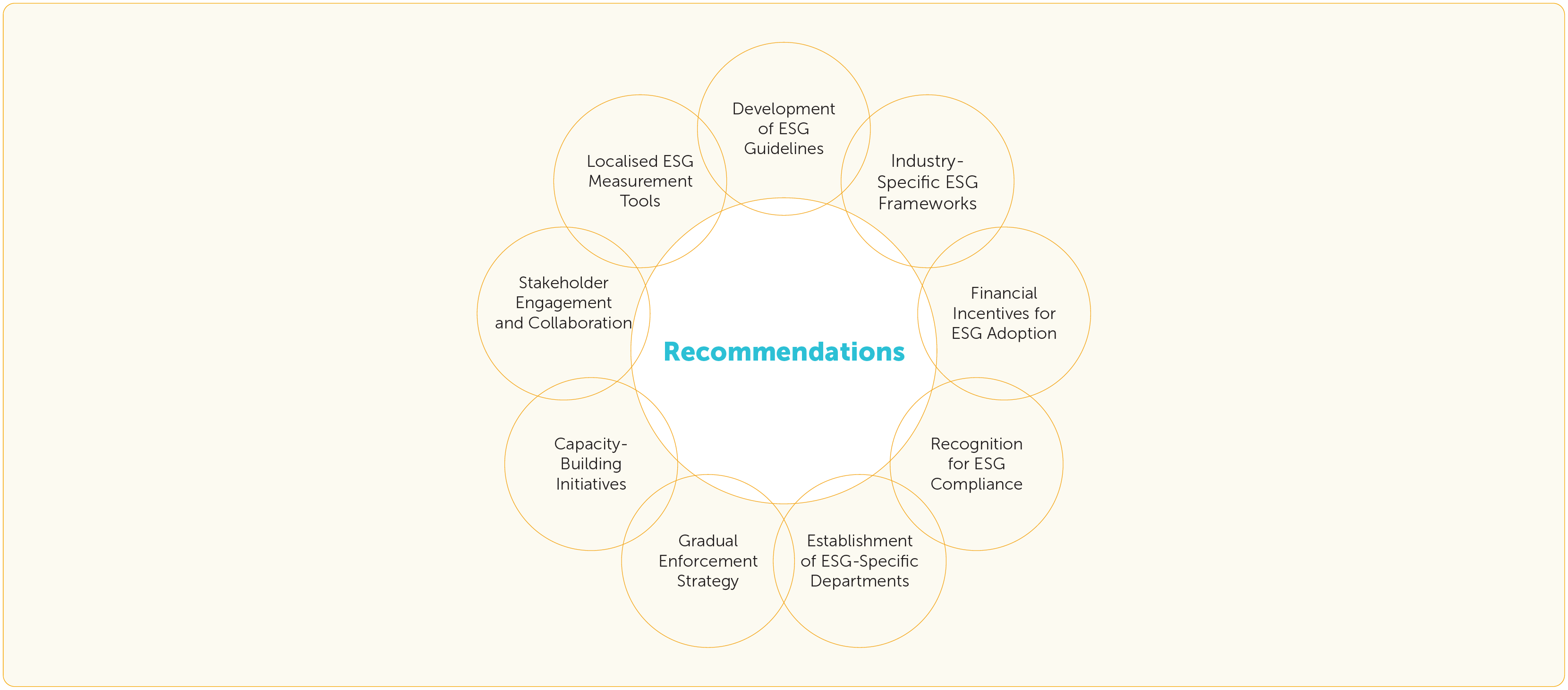

Recommendations

The findings of this study provide a comprehensive understanding of ESG implementation across different organisational contexts, particularly among SMEs and larger companies. The analysis highlights key challenges and disparities in ESG adoption, including fragmented implementation, resource constraints, and the absence of industry-specific ESG tools. Addressing these challenges requires a multi-faceted approach involving policy interventions, financial incentives, capacity-building initiatives, and enhanced stakeholder engagement. The following recommendations outline actionable strategies to promote ESG adoption across industries:

1. Standardised ESG Guidelines

A national ESG framework with clear rules is needed. Many SMEs already follow ESG-friendly practices but lack awareness. Awareness campaigns can help businesses understand the benefits of ESG adoption.

2. Industry-Specific ESG Frameworks

Different industries have unique ESG challenges, so tailored frameworks are necessary. For example, waste management is a major issue for industrial sectors, requiring specialised solutions.

3. Financial Incentives

ESG adoption is costly, especially for SMEs. Offering tax breaks, grants, and low-interest loans can encourage compliance. Government-funded training can also help businesses implement ESG strategies.

4. Recognition for ESG Compliance

Public recognition through certifications and awards can motivate businesses. Many SMEs engage in ESG practices but do not report them, missing opportunities for credibility and investment.

5. Dedicated ESG Departments

Large companies have structured ESG programmes, but SMEs lack formal governance. Establishing ESG teams can improve strategy integration, compliance, and reporting accuracy.

6. Gradual Enforcement

ESG compliance should be introduced in phases to ease the burden on SMEs. A step-by-step approach will help businesses transition without disrupting operations.

7. Capacity-Building Initiatives

Many SMEs lack ESG knowledge. Training programmes, workshops, and partnerships with universities can help businesses understand and implement sustainable practices.

8. Stakeholder Engagement

Collaboration with employees, investors, and communities is key. Industry associations and online platforms can help SMEs share best practices and strengthen ESG efforts.

9. Simplified ESG Metrics

Current ESG measurement tools are too complex for SMEs. Developing localised tools will help businesses track progress in areas like carbon footprint, diversity, and governance compliance.

Figure 11: The recommendations for this research.

The successful adoption of ESG practices among SMEs requires a holistic and tailored approach that acknowledges their unique constraints and operational realities. Simplified ESG guidelines, financial incentives, capacity-building efforts, stakeholder engagement, and localised measurement tools are crucial in fostering consistent and meaningful ESG adoption. Through targeted support and collaboration, SMEs can overcome ESG implementation barriers, contribute to sustainability objectives, and enhance their long-term competitiveness and resilience. Addressing these challenges is critical not only for equitable ESG adoption but also for ensuring sustainable economic growth and global alignment in ESG standards.

Conclusion

This study explores the challenges, resource allocation strategies, and assessment frameworks for ESG adoption among SMEs, revealing disparities driven by resource constraints, regulatory demands, and stakeholder pressure. SMEs, comprising 98.4 per cent of the sample, focus on governance and social factors for compliance and workforce stability, while environmental efforts remain limited due to high costs and non-mandatory reporting. In contrast, larger companies adopt structured ESG strategies aligned with international frameworks like GRI and CDP. The study underscores the influence of organisational characteristics, stakeholders, and operational constraints on ESG adoption, emphasising the dominance of governance. To bridge these gaps, it recommends simplified ESG guidelines, financial incentives, capacity-building programmes, stakeholder engagement, and localised measurement tools. Achieving widespread ESG adoption requires targeted support, collaboration, and long-term commitment, ultimately enhancing ESG performance, aligning organisations with global standards, and fostering sustainability-driven resilience and competitiveness.

References

Agosto, A., Giudici, P., & Tanda, A. (2023).

How to combine ESG scores? A proposal based on credit rating prediction. https://doi.org/10.1002/csr.2548.

Ang, G., Guo, Z., & Lim, E.-P. (2023).

On Predicting ESG Ratings Using Dynamic Company Networks. ACM Transactions on Management Information Systems, 14(3), 1–34. https://doi.org/10.1145/3607874.

Dai, T., & Tang, C. (2022).

Frontiers in Service Science: Integrating ESG Measures and Supply Chain Management: Research Opportunities in the Postpandemic Era. Service Science, 14(1), 1–12. https://doi.org/10.1287/serv.2021.0295.

Dmuchowski, P., Dmuchowski, W., Baczewska-Dąbrowska, A. H., & Gworek, B. (2023).

Environmental, social, and governance (ESG) model; impacts and sustainable investment – Global trends and Poland's perspective. Journal of Environmental Management, 329(117023), 117023. https://doi.org/10.1016/j.jenvman.2022.117023.

Fatemi, A., Glaum, M. & Kaiser, S. (2018).

ESG performance and firm value: The moderating role of disclosure. Global Finance Journal, Elsevier, 38(C), 45-64.

Jegatheswaran Ratnasingam, Hazirah Ab Latib, Lim Choon Liat, Natkuncaran Jegatheswaran, Othman, K., & Mohd Afthar Amir. (2023).

Environmental, social, and governance adoption in the Malaysian wood products and furniture industries: Awareness, adoption, and challenges. Bioresources, 18(1), 1436–1453. https://doi.org/10.15376/biores.18.1.1436-1453.

Mohd Taib, N., & Haron, R. (2024).

The Overview of Environment, Social, And Governance Practices Among Malaysian Companies. In Insight Journal Vol. 11, Issue 2). https://doi.org/https://doi.org/10.24191/ij.v11i2.

Rangel, R., Batista, V., & Alcabiades Negrao Macedo. (2024).

Validation of Challenges for Implementing ESG in the Construction Industry Considering the Context of an Emerging Economy Country. Applied Sciences, 14(14), 6024–6024. https://doi.org/10.3390/app14146024.

Vivoda, V. & Matthews, R. (2023).

"Friend-shoring" as a panacea to Western critical mineral supply chain vulnerabilities. Mineral Economics. https://doi.org/10.1007/s13563- 023-00402-1.

Wang, L. (2024).

Challenges and Opportunities of ESG Integration in Financial Operations, Modern Management Science & Engineering, 6(1), p162–p162. https://doi.org/10.22158/mmse.v6n1p162.

Wu, Y., & Tham, J. (2023).

The Impact of Executive Green Incentives and Top Management Team Characteristics on Corporate Value in China: The Mediating Role of Environment, Social and Government Performance. Sustainability, 15(16), 12518–12518. https://doi.org/10.3390/su151612518.

Zhang, A., & Zhang, J. H. (2023).

Renovation in environmental, social and governance (ESG) research: the application of machine learning. Asian Review of Accounting. https://doi.org/10.1108/ara-07-2023-0201.