TOPIC

09

Streamlining Cashless Adoption in Malaysia: An Evaluation of MCMC's Cashless Society Programme Effectiveness and Impact

LEAD RESEARCHER

Assoc. Prof Dr. Rahayu Ahmad

UNIVERSITI UTARA MALAYSIA

TEAM MEMBERS

Dr. Syahida Hassan

UNIVERSITI UTARA MALAYSIA

Abstract

This research critically evaluates the Cashless Society Programme (CSP) organised by the Malaysian Communications and Multimedia Commission (MCMC), examining its implementation, alignment with national strategies, impact on bridging the digital divide, and potential for collaboration with other initiatives. A survey of 344 respondents was conducted during the CSP in Johor, Negeri Sembilan, and Pahang, alongside content analysis and focus groups with key stakeholders. The findings revealed that CSP has positively impacted society, with 50 per cent of respondents intending to continue using cashless payments. However, challenges remain, particularly for the elderly, who face barriers such as computer anxiety, lack of technical skills, and concerns about fraud. The study suggests further investigations into these issues and calls for more inclusive research.

The CSP aligns with national strategies like MyDIGITAL, Ekonomi MADANI, and Bank Negara Malaysia's Financial Sector Blueprint 2022-2026, supporting digital inclusion, financial literacy, and collaboration among stakeholders. Despite progress in digitalisation and economic competitiveness, gaps in outreach and evaluation mechanisms persist. The study proposes an evaluation framework with key performance indicators (KPIs) for better planning, implementation, and outcomes. It also identifies gaps in cashless initiatives and suggests complementary programmes like Ecosystem-based Awareness for MSMEs and the elderly. The findings underscore the need for targeted programmes, robust evaluation, and collaborative efforts to ensure a secure, inclusive, and efficient cashless payment ecosystem in Malaysia.

Keywords: Cashless payment, Malaysia, digital divide

Introduction

The Ekonomi MADANI, MyDIGITAL, and the Financial Sector Blueprint 2022 - 2026, collectively highlight the importance of adopting cashless transactions to help realise the goal of the digital economy contributing 25.5 per cent to GDP by 2025. This has led to the initiation of numerous cashless projects within multiple government entities. For example, the Malaysian Communications and Multimedia Commission (MCMC) has collaborated with strategic partners such as Payments Network Malaysia Sdn. Bhd. (PayNet) as well as FSPs including TNG Digital Sdn. Bhd., Axiata Digital Ecode Sdn. Bhd. (Boost), Maybank and Delivery Hero Malaysia Sdn. Bhd. (Foodpanda) to encourage traders to register their businesses with Financial Service Providers (FSPs) or digital platform providers to facilitate the cashless payment process. The partners were extended in phase two (2), the Cashless Society Programme, by including FELDA, Sakupay, TNG, Setel, Maybank, UUM, BNM, BSN, BIMB, AKPK, TMUnifi and State Government agencies. There is a need to examine the impact of the cashless society programmes that have been implemented to ensure sustained motivation to use cashless payment. Additionally, there is a need to investigate the alignment or the overlapping initiatives by these various agencies. This is important to promote efficiency and consistency: When multiple agencies are working towards the same goal of promoting cashless transactions, it's essential to ensure that their efforts are aligned. This alignment helps in streamlining processes, avoiding duplication of efforts, and maximise resources. It ensures that initiatives complement each other rather than conflicting or working at cross-purposes.

The following are the objectives of the research:

To analyse CSP implementation and effectiveness.

To evaluate CSP alignment and contribution.

To investigate CSP's impact in addressing the digital divide.

To identify similar or potentially complementary programmes and recommend collaboration.

Literature Review

Financial Sector Blueprint 2022-2026 by Bank Negara Malaysia

The financial blueprint by Bank Negara Malaysia for 2022-2026 focuses on strengthening Malaysia's financial sector to support sustainable economic growth, with an emphasis on digital transformation, financial inclusion and enhancing financial stability. It outlines strategic initiatives to promote innovation in financial services, improve regulatory frameworks, and ensure a more resilient, inclusive, and dynamic financial ecosystem. The blueprint has outlined five (5) strategic thrusts:

Fund Malaysia's economic transformation

Elevate the financial well-being of households and businesses

Advanced digitalisation of the financial sector

Position the financial system to facilitate an orderly transition to a greener economy

Advance value-based finance through Islamic finance leadership by sharpening Malaysia's proposition as an international gateway for Islamic finance

The initiative for cashless payment is under the provisions of Thrust 2 and Thrust 3. Under thrust 3, strategies include supporting a more vibrant digital financial services landscape and supporting industry-led strategies for digital payments adoption. In recent years, the industry has become increasingly competitive, particularly with the influx of new players, leading to more affordable and innovative services for merchants, including SMEs. Advances in consumer-facing technologies, such as biometrics and wearables, have also enhanced the convenience of digital payments.

BNM will support industry-driven strategies to foster digital payment adoption and will review current regulatory frameworks to ensure their continued relevance. These include the e-Payment Incentive Fund Framework (ePIF), the Payment Card Reform Framework (PCRF), and the Interoperable Credit Transfer Framework (ICTF).

The financial blueprint aligns with the broader national aspirations for digital payments under MyDigital. Federal and state agencies' commitment to cashless payments plays a pivotal role in creating behavioural shifts towards greater digital payment adoption.

Ekonomi Madani

Ekonomi Madani is Malaysia's vision for a sustainable and inclusive economy that emphasises social well-being, equitable growth, and environmental responsibility. It focuses on creating a fairer society through inclusive policies, enhancing the welfare of all Malaysians, and fostering innovation and digital transformation while ensuring economic sustainability and resilience for future generations. The Madani economy has outlined four (4) thrusts;

Thrust 1: Raising the Ceiling,

%20--%3e%3csvg%20version='1.1'%20id='Layer_1'%20xmlns='http://www.w3.org/2000/svg'%20xmlns:xlink='http://www.w3.org/1999/xlink'%20x='0px'%20y='0px'%20viewBox='0%200%2019%2019'%20style='enable-background:new%200%200%2019%2019;'%20xml:space='preserve'%3e%3cstyle%20type='text/css'%3e%20.st0{fill:%232DC1D6;}%20.st1{fill:%23FFFFFF;}%20%3c/style%3e%3cg%3e%3cg%3e%3cpath%20class='st0'%20d='M9.5,19C4.3,19,0,14.7,0,9.5S4.3,0,9.5,0S19,4.3,19,9.5S14.7,19,9.5,19'/%3e%3c/g%3e%3cpolygon%20class='st1'%20points='4.9,5.7%205.8,5.3%209.5,12.6%2013.2,5.3%2014.1,5.7%2010,13.7%209,13.7%20'/%3e%3c/g%3e%3c/svg%3e)

Thrust 2: Enhancing Governance, and

Thrust 3: Elevating the Floor

In relation to digital services and payment, there are several initiatives under each thrust. Under Thrust 1, the PMKS Digitalisation Grant assists SMEs in adopting digital services for their daily business operations. Meanwhile, in Thrust 2, the emphasis is on the delivery of agile and collaborative public services. This includes facilitating the delivery of public services and enhancing the Government's capabilities through the digitalisation agenda to the highest level.

MyDigital

MyDIGITAL embodies the Government's vision to elevate Malaysia into a high-income nation fuelled by digitalisation and technology, aiming to establish regional leadership in the digital economy. It promotes the participation and use of digital and cashless transactions to both users and traders to form a cashless society and spur the nation's digital economy. Among the targets for Malaysia in 2025 is: 22.6 per cent of the digital economy to Malaysia's 875,000 micro, small and medium enterprises (MSMEs) adopt eCommerce. In addition, the Ministry of Finance (MoF) is committed to transitioning all government service payments to a cashless system by 2022. The targets will be achieved through six (6) strategic thrusts and 22 strategies. The six (6) thrusts are:

Drive the digital transformation in the public sector,

Boost economic competitiveness through digitalisation,

Build enabling digital infrastructure,

Build agile and competent digital talent,

Create an inclusive digital society, and

Build trusted, secure and ethical digital environment

In relation to cashless payment, the focus will be on Thrusts 5 and 6. Several strategies are deployed, including increasing the inclusivity of all Malaysians in digital activities and strengthening safety and ethics in digital activities and transactions. Specific targets related to cashless payment include having 400 electronic payment transactions made per capita and 36 Electronic Fund Transfer Point of Sales (EFTPOS) terminals per 1,000 inhabitants by 2022.

Cashless Society Framework

The Cashless Society Framework by the Malaysian Communications and Multimedia Commission (MCMC) is designed to facilitate the transition towards a cashless economy in Malaysia by promoting digital payment adoption across all sectors. The objective is to create a sustainable, thriving, informed, cashless society for the local communities. There are two (2) main tracks under this framework: Framework: 1) Policy intervention and implementation by the state government and relevant agencies, and 2) Implementation of digital premises by promoting MSMEs to adopt digital platforms and having a digital presence.

There are four pillars supporting this framework:

Namely digital literacy

Security and Safety

Income Opportunity

Capacity Building

Digital literacy aims to facilitate financial inclusion by ensuring everyone, regardless of socioeconomic status, has access to digital financial services. In addition, implementing awareness programmes on the effective use of digital technology and promoting the use of cashless technology. Under the second pillar, MCMC aims to increase awareness of the current challenges of digital transactions. In addition, MCMC also promotes secure/safe use of digital transactions, fraud prevention and data privacy. Meanwhile, the third pillar emphasises awareness for people to generate income within the digital realm. The fourth pillar aims to focus on capacity-building programmes and training for online purchases/ digital transactions. The indicators for the successful rollout of this framework are the number of digitally ready community touchpoints, the number of cashless payments transacted and the number of traders on board on digital platforms.

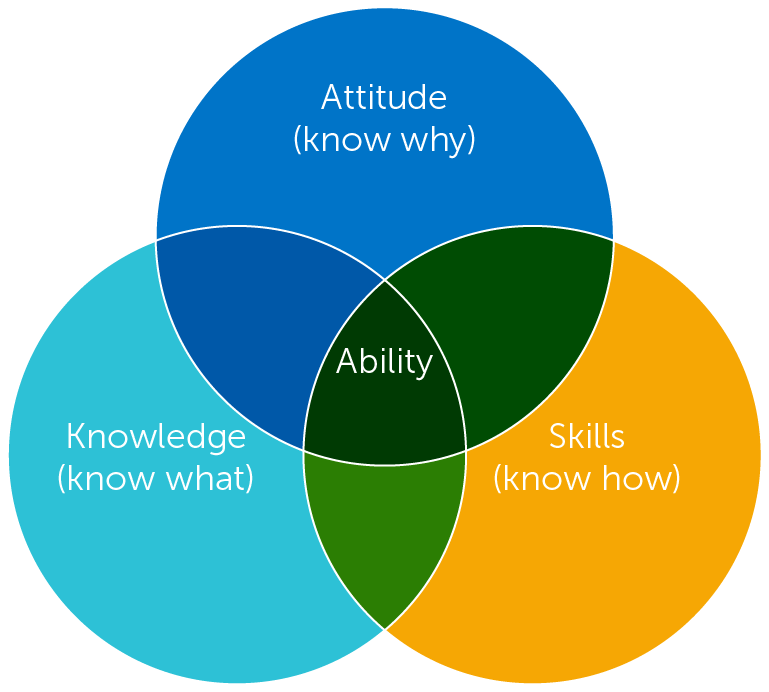

KSA Model

Aligning with MCMC's four (4) pillars; a) Digital and Financial Literacy, b) Security and Safety, c) Income, and d) Capacity Building), the Knowledge Skills Attitude (KSA) model (see Figure 1) can be used to examine the effectiveness of the cashless programme in developing civilians' skills in pursuing digital economy. According to the KSA model, knowledge refers to the cognitive process of mental skills. Attitude is with feelings or emotions, and skills are the psychomotor process of manual or physical skills (Anderson, Krathwohl, Airasian, Cruikshank, Mayer, Pintrich, Raths & Wittrock, 2000). In relation to digital payment, attitude can be represented by users' intentions or preferences in using digital payment. Meanwhile, knowledge can be represented by competencies in using and managing digital payment inclusive of financial and digital literacy, security and safety. Skills can be operationalised as the ability to locate and use the key features in digital payment apps or digital wallets. The KSA model is embedded in the survey questions and will be distributed during the cashless programme in Johor, Negeri Sembilan and Pahang. There were 17 locations in Pahang, 21 in Johor and 51 in Negeri Sembilan.

Figure 1: The KSA Model.

Methodology

This section presents the methodology of the research. Figure 2 shows the relationship between the research objectives and the methodology adopted for this study.

Data Collection

Two main data collection techniques are used for this study: survey and focus group. The survey is employed to address Research Objective 1 and Research Objective 3, while the focus group session is conducted to fulfil Research Objective 2 and Research Objective 4.

Survey During the CSP Programme

In conjunction with the MCMC Cashless Society Programme (CSP), surveys are conducted at selected locations in three (3) states: Johor, Negeri Sembilan and Pahang. These locations are chosen because they have a digital blueprint, high broadband coverage and more than 95 per cent network availability. Some programmes are organised at selected NADI centres based on criteria such as the number of residents, the number of entrepreneurs within the area, distance from the nearest town, suitability of the compound for organising the programme, broadband coverage and availability of public halls.

RO1: To analyse CSP implementation and effectiveness.

%20--%3e%3csvg%20version='1.1'%20id='Layer_1'%20xmlns='http://www.w3.org/2000/svg'%20xmlns:xlink='http://www.w3.org/1999/xlink'%20x='0px'%20y='0px'%20viewBox='0%200%2019%2019'%20style='enable-background:new%200%200%2019%2019;'%20xml:space='preserve'%3e%3cstyle%20type='text/css'%3e%20.st0{fill:%232DC1D6;}%20.st1{fill:%23FFFFFF;}%20%3c/style%3e%3cg%3e%3cg%3e%3cpath%20class='st0'%20d='M19,9.5c0,5.2-4.3,9.5-9.5,9.5S0,14.7,0,9.5C0,4.3,4.3,0,9.5,0S19,4.3,19,9.5'/%3e%3c/g%3e%3cpolygon%20class='st1'%20points='5.7,14.1%205.3,13.2%2012.6,9.5%205.3,5.8%205.7,4.9%2013.7,9%2013.7,10%20'/%3e%3c/g%3e%3c/svg%3e)

Survey during CSP in Johor, Negeri Sembilan, and Pahang.

- Rate of cashless use among users and merchants

- Rate of continuous use of cashless

- Impact of cashless use

RO2: To evaluate CSP alignment and contribution with national cashless society strategies.

Literature Review and Focus Group with key players in cashless agenda.

Alignment Matrix demonstrate unique and overlapping CSP by different agencies.

RO3: To investigate CSP's impact in addressing the digital divide.

Survey during CSP in Johor, Negeri Sembilan, Pahang and online survey in online communities.

Rate of digital divide in terms of skills, knowledge, and usage of cashless.

RO4: To identify similar or potentially complementary programmes.

Literature Analysis and Interview and brainstorming in focus group session.

Collaborative cashless programmes among multiple agencies.

Figure 2: The research framework.

During the CSP programme, participants stand the chance to win a lucky draw upon completing the survey. The online survey will consist of questions regarding the frequency and types of cashless payments used, factors influencing the usage of cashless, and participants' continuous intention to use cashless payments. Additionally, there are questions that examine the impact of cashless in generating income opportunities.

There are two (2) sets of surveys: one for users and the other for merchants. For the merchant survey, questions focus on the impact of digital wallets on merchants' financial and business management and on retaining their customers. In addition to the surveys distributed during the cashless society programme, online surveys are also advertised in merchants' community groups and social media platforms.

Focus Group Session

In fulfilling research objectives 2 and 4, a focus group session is conducted. Prior to this session, a literature review was conducted to compile related cashless initiatives by various agencies, state government and financial service providers. The analysis is classified into different segments. The analysis for each stakeholder was shared via email along with the invitation to attend the focus group. Five (5) organisations participated in the focus group, which was held on 7 November 2024 at Primeira Hotel, Kuala Lumpur. MCMC, Bank Negara Malaysia, Bank Simpanan Nasional, Negeri Sembilan State and Sakupay were among the organisations that participated in the session. The focus group began with a briefing from the researcher team on the analysis of cashless initiatives. Then, several follow-up questions were brought up during the session to clarify the initiatives. The feedback from the focus group was used to refine the initial analysis on the alignment of cashless initiatives.

The questions focused on:

Understanding the implementation of the initiatives,

The success and challenges of the programme, and

The target audience for the programme

Findings and Analysis

This section begins by illustrating the distribution of the respondents by state. Then, the demographics of the respondents are presented. The distribution of the respondents is demonstrated in the table below.

| State | Period of Data Collection | Number of respondents |

|---|---|---|

| Johor | 21/02/2024 – 10/03/2024 | 109 |

| Negeri Sembilan | 07/06/2024 – 03/08/2024 | 125 |

| Pahang | 11/09/2024 – 08/10/2024 | 125 |

| Total | 344 | |

Table 1: The Distribution of the Respondents.

The analysis for Johor is conducted separately as data was collected in the early period. Some revisions have been made for the consecutive data collection in Negeri Sembilan and Pahang.

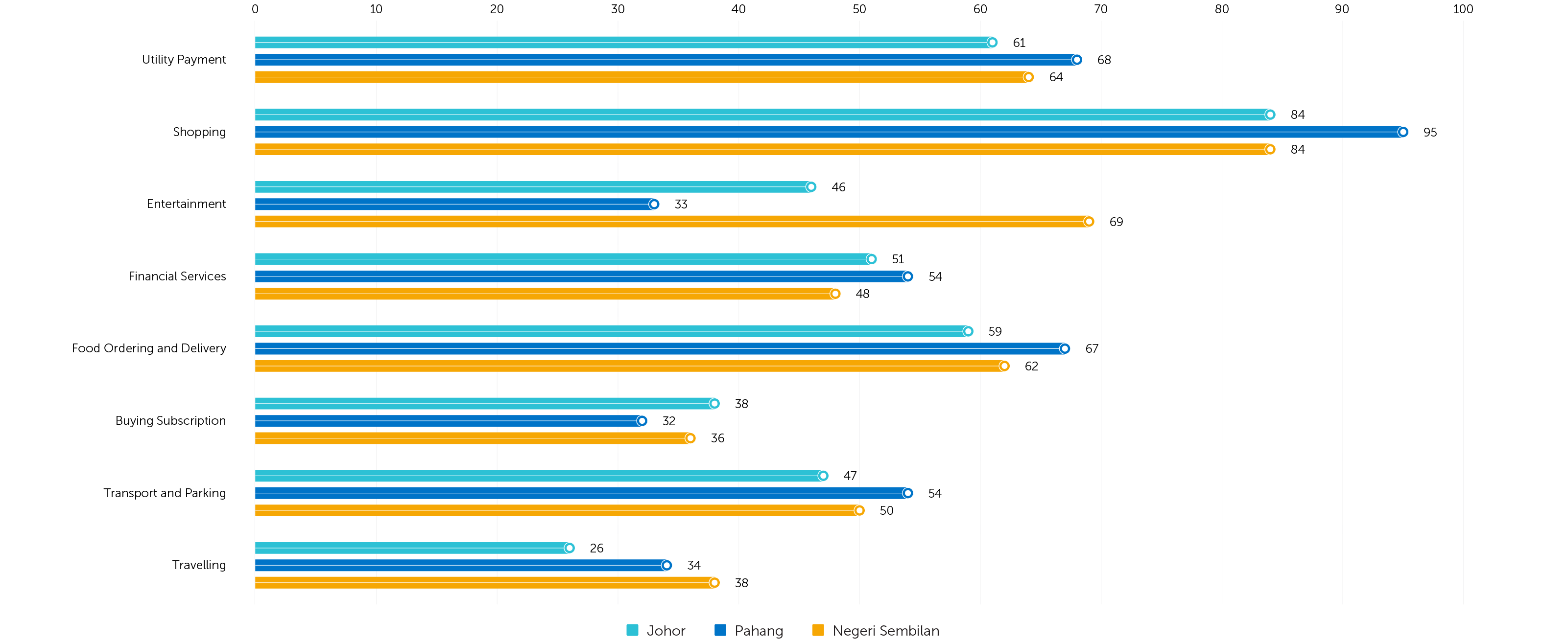

The respondents were composed of 60 per cent (N=195) female and 40 per cent male (N=59). 40 per cent (N=130) of the respondents aged between 26 to 35, followed by 30 per cent in the aged between 36 to 44. respondents aged between 18 to 25 constitute 20 per cent of the respondents. In terms of education, 40 per cent are SPM holders (n= 131), followed by Diploma and Degree, 30 per cent each. As for income, 40 per cent earn between RM1,500 to RM3,000, and another 30 per cent earn below RM1,500. QR Pay (any bank), Touch n Go, and ShopeePay are the top three (3) types of cashless payment frequently among the respondents. Figure 2 below shows the popular cashless payment usage across the three states. The top three cashless payment usages are shopping, utility payment and food ordering.

Cashless Payment Usage

Figure 3: Cashless payment usage.

Findings for Research Objective 1

To measure the success of the Cashless Society Programme (CSP) Implementation and Eectiveness several metrics were used. There are analyses provided for each state, namely: 1) Knowledge of the Safety of Cashless Payment (knowledge), 2) Perception of Cashless Payment Eectiveness, and 3) Continuous Intention to use Cashless Payment (attitude).

Knowledge of the Safety of Cashless Payment

a) Johor

Knowledge of Cashless Payment Safety

Figure 4: Knowledge of cashless payment safety (Johor).

Figure 4 above shows that almost half of the Johor respondents (49.4 per cent, N=109) agreed that cashless payments have safety features, such as notification each time a transaction is performed and biometric identification through fingerprints, etc.

b) Pahang and Negeri Sembilan

Knowledge of Cashless Payment Safety

Figure 5: Knowledge of Cashless Payment Safety.

In comparison among Pahang and Negeri Sembilan respondents, both states have similar distributions in which approximately 80 per cent agreed that cashless payments have safety features through notification each time a transaction is performed and biometric identification through fingerprints, etc., as shown in Figure 5.

Perception of Cashless Payment Effectiveness

a) Johor

Figure 6 shows that approximately 56 per cent (N=61) of Johor respondents agreed that cashless payment is an effective method of performing their financial transactions.

Perception of Cashless Payment Effectiveness

Figure 6: Perception of Cashless Payment Effectiveness.

b) Pahang and Negeri Sembilan

Perception of Cashless Payment Effectiveness

Figure 7: Perception of Cashless Payment Effectiveness.

As demonstrated in Figure 7, both Pahang and Negeri Sembilan have a proportionate distribution of responses for the perception of cashless effectiveness. Almost 88 per cent of Pahang and Negeri Sembilan respondents perceived that cashless payment allows them to perform financial transactions faster and more effectively.

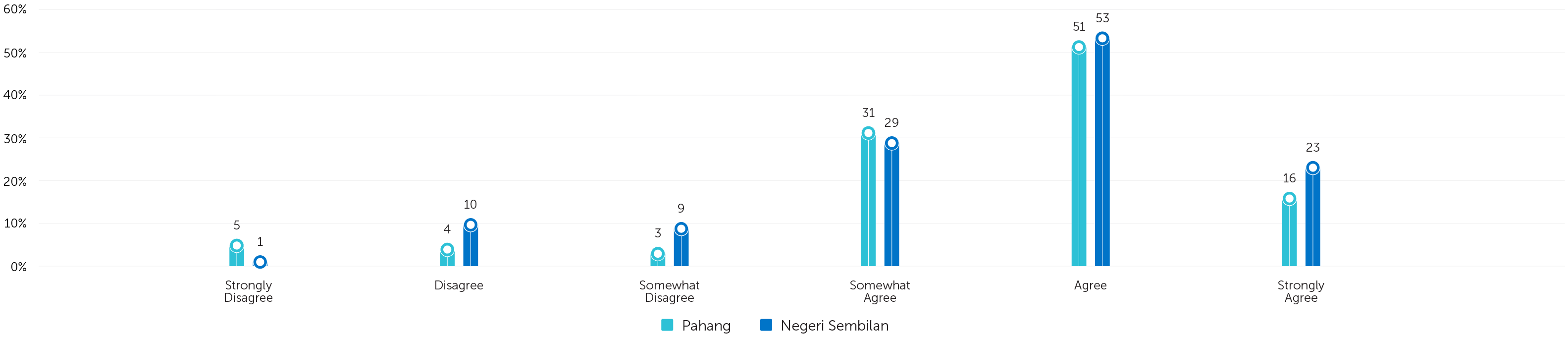

Continuous Intention to Use Cashless Payment

a) Johor

Continuous Intention to Use Cashless Payment

Figure 8: Continuous Intention to Use Cashless Payment.

b) Pahang and Negeri Sembilan

Continuous Intention to Use Cashless Payment

Figure 9: Continuous Intention to Use Cashless Payment.

Figure 9 shows that Negeri Sembilan has a slightly larger proportion (59 per cent) of respondents who agree to continue using cashless payments than Pahang. In comparison, 41 per cent of Pahang respondents agree to continue using cashless payments.

In conclusion, the impact of CSP is positive as attributed to the level of knowledge regarding cashless payment safety and the favourable perception of cashless payment effectiveness. Most respondents (80 per cent) agreed cashless payments have safety features through notification each time a transaction is performed and biometric identification through fingerprints. They also (60 to 80 per cent) regarded cashless payments as an effective method for financial transactions allowing them to perform financial transactions faster and more effectively. In addition, the future for cashless payment looks promising, as almost half of the respondents surveyed would like to continue using cashless payment in the future.

Findings for Research Objective 2

The following table is the result of content analysis comparing the alignment of MCMC CSP programmes with the main digital payment frameworks: My Digital, Ekonomi Madani, and Malaysia's Financial Sector Blueprint.

| MCMC CSPs Programmes | MyDigital | Ekonomi Madani | Malaysia’s Financial Sector Blueprint | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Thrust 2 | Thrust 4 | Thrust 5 | Thrust 6 | Thrust 1 | Thrust 2 | Thrust 1 | Thrust 2 | Thrust 3 | |

| MCMC CSPs Programmes | %20--%3e%3csvg%20version='1.1'%20id='Layer_1'%20xmlns='http://www.w3.org/2000/svg'%20xmlns:xlink='http://www.w3.org/1999/xlink'%20x='0px'%20y='0px'%20viewBox='0%200%2030%2030'%20style='enable-background:new%200%200%2030%2030;'%20xml:space='preserve'%3e%3cstyle%20type='text/css'%3e%20.st0{fill:%232DC1D6;}%20.st1{fill:%23FFFFFF;}%20%3c/style%3e%3cg%3e%3cpath%20class='st0'%20d='M30,15c0,7.2-5.1,13.3-11.9,14.7c-1,0.2-2,0.3-3.1,0.3C6.7,30,0,23.3,0,15C0,6.7,6.7,0,15,0%20c8.1,0,14.7,6.4,15,14.4C30,14.6,30,14.8,30,15'/%3e%3cpath%20class='st1'%20d='M23.4,9.7c-0.8-0.8-2.2-0.8-3.1,0l-7.4,7.4L9.8,14c-0.8-0.8-2.2-0.8-3.1,0c-0.8,0.9-0.8,2.2,0,3.1l4.7,4.7%20c0.4,0.4,1,0.6,1.5,0.6c0.6,0,1.1-0.2,1.5-0.6l9-9C24.3,11.9,24.3,10.5,23.4,9.7'/%3e%3c/g%3e%3c/svg%3e) |

|

|||||||

| Digital & Financial literacy | |

|

|

|

|||||

| Safety and Security | |

|

|

||||||

| Capacity Building | |

|

|

||||||

| Income Opportunity | |

|

|

|

|||||

| Legend: |

My Digital - Thrust 2: Boost economic competitiveness through digitalisation My Digital - Thrust 4: Build agile and competent digital talent My Digital - Thrust 5: Create an inclusive digital society My Digital - Thrust 6: Build a trusted, secure and ethical digital environment. Ekonomi Madani - Thrust 1: Raise the ceiling Ekonomi Madani - Thrust 2: Raise the floor FSB - Thrust 1: Fund Malaysia's Economic Transformation FSB - Trust 2: Elevate the Financial Well-being of Households and Businesses FSB- Trust 3: Advance Digitalisation of the Financial Sector |

||||||||

Table 2: MCMC CSP's programme alignment with national cashless society strategies and its contribution to national blueprints.

The following table demonstrates the comparison between MCMC programmes and the key stakeholders in cashless payment, namely, Bank Negara Malaysia (BNM), MDEC, and PayNet. The comparison is based on several metrics, such as the location of the programmes, the target audience, the policy coverage, and the incentives provided.

| Complementary Aspects of MCMC | MCMC | BNM | MDEC | PayNet |

|---|---|---|---|---|

| Complementary Aspects of MCMC | FELDA settlers and NADI centres | Rural, Specific Island | Mall | Educational Institutions and Local Markets |

| Target Audience | Merchants | Merchants | Merchants | Merchants and users |

| Policy | State Level | National Level | No policy | No policy |

| Incentives | Lucky Draw during CSP Programmes In-kind incentives by strategic partners | Provide shared payment infrastructure | Grants | Discount & Rewards |

Table 3: MCMC CSP's programme alignment with national cashless society strategies and its contribution to national blueprints.

Findings for Research Objective 3

For research objective 3, analysis was carried out to investigate the impact of CSP in addressing the digital divide. The metrics used are 1) General Technical Expertise (skills) and 2) Perception of Cashless Payment Benefits (attitude).

General Technical Expertise

Figure 10 shows that most respondents were neutral when asked about their skills in using smartphones, applications, websites, or computer programmes. Approximately 35 per cent of the respondents answered neutral for all the questions.

General Technical Expertise (Johor)

-01.png)

Figure 10: General Technical Expertise (Johor).

Meanwhile, for Pahang, Figure 11 shows that approximately 50 per cent of the respondents disagree that they have difficulties when using smartphones, applications, websites, or computer programmes. They perceive themselves as capable of solving problems independently related to device usage.

General Technical Expertise (Pahang)

-01.png)

Figure 11: General Technical Expertise (Pahang).

Based on Figure 12, approximately 60 per cent of the respondents disagree that they have difficulties using smartphones, applications, websites, or computer programmes. They perceive themselves as capable of solving problems independently related to device usage.

General Technical Expertise (Negeri Sembilan)

-01.png)

Figure 12: General Technical Expertise (Negeri Sembilan).

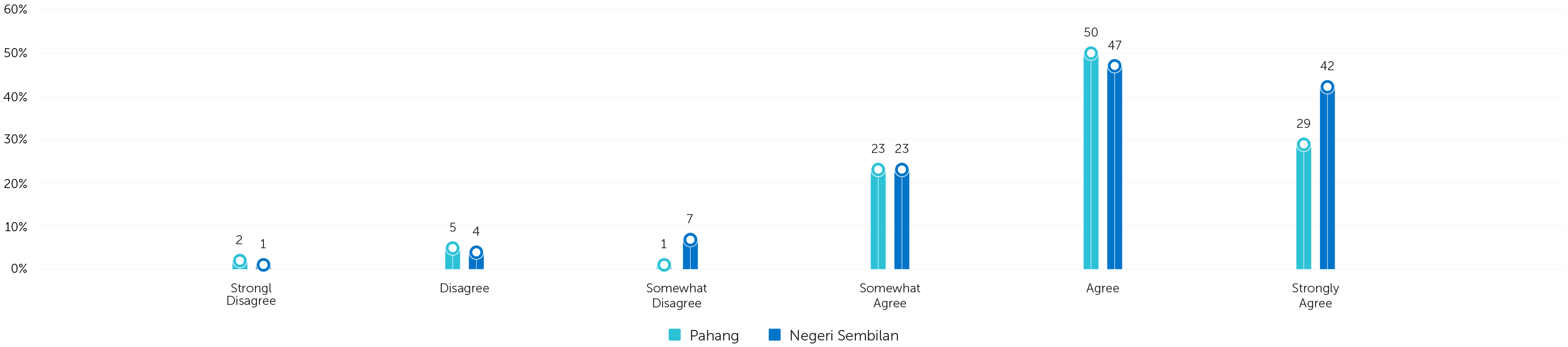

Perception of Cashless Payment Benefit

Perception of Cashless Payment Benefit

Figure 13: Perception of Cashless Payment Benefit

Figure 13 above displays an almost equal distribution of the percentages of Pahang and Negeri Sembilan respondents who have positive perceptions of the cashless payment benefit. The benefits perceived include reduced time for financial transactions and instant or real-time access to online financial services.

Findings for Research Objective 4

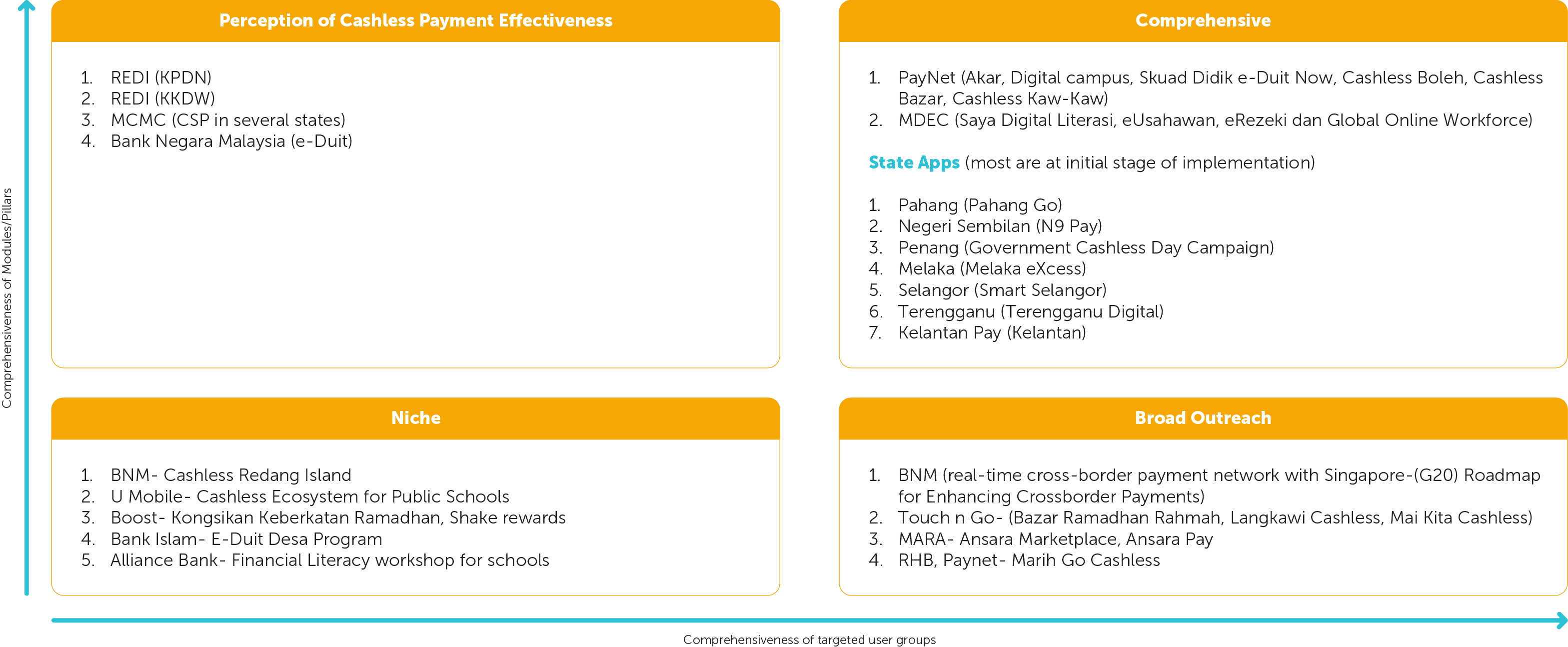

For this research objective, this study analyses and classifies existing cashless initiatives in Malaysia, offering a structured overview of the various programmes. Subsequently, the section delves into the stakeholders involved, including agencies, state governments, ministries, financial institutions, and their related policies and incentives. This is followed by an assessment of these initiatives using a quadrant categorisation framework to evaluate their comprehensiveness and outreach. Each quadrant helps categorise programmes based on their scope and user focus as the following:

1. Targeted Quadrant (Top-Left):

Programmes in this quadrant focus on specific user groups with a relatively narrow range of modules/pillars.

2. Comprehensive Quadrant (Top-Right):

These programmes cover a broad range of modules or pillars (e.g., digital literacy, financial inclusion, capacity building) and aim to reach multiple types of user groups (merchants and users) regardless of state or national level.

3. Niche Quadrant (Bottom-Left):

These initiatives are narrow in both scope and audience, focusing on specific needs or unique user groups but addressing them thoroughly.

4. Broad Outreach Quadrant (Bottom-Right):

Programmes in this quadrant target a wide range of user groups but are less comprehensive in terms of the number of modules or pillars covered.

Figure 14: Quadrant Categorisation of Cashless Payment Awareness Programmes in Malaysia.

Recommendations

For research objective one, the population covered in this study is mostly between the ages of 26 and 35. As Malaysia is striving for financial inclusion, it is imperative to focus specifically on the impact on elderly groups. Future studies should examine the specific barriers this group faces. These barriers include technological, psychological, physical and cognitive risk and data collection challenges. For future research, data collection among the elderly should be meticulously planned. A more personalised and accessible approach is advisable, such as conducting interviews instead of relying solely on survey methods. Interviews can offer deeper insights into the specific challenges faced by elderly individuals, enabling more effective customisation of the CSP to meet their needs. In addition, the data collected from merchants in this study is insufficient to draw meaningful and valid conclusions. MCMC, in collaboration with Bank Negara and financial service providers, could undertake a nationwide study to examine the factors influencing the adoption of cashless payments among merchants. Enumerators can be appointed in each state to distribute surveys to selected MSMEs. Future studies could also complement the surveys with interviews to gain a deeper understanding of the challenges merchants face and to address any misconceptions.

For research objective two, the analysis has presented the alignment of MCMC initiatives with national financial blueprints. The MCMC's CSP has made significant contributions to advancing Malaysia's cashless society goals. It supports digital transformation, enhances financial inclusion, and strengthens Malaysia's competitiveness in the regional digital economy. However, to maximise its impact and alignment with national strategies, a robust monitoring framework needs to be implemented, which includes the phases below:

a) Planning stage

Roundtable sessions can be conducted among relevant agencies; financial service providers and state government can outline the number of programmes or training sessions that can be conducted. The objective, target groups, modules and alignment to the national policies need to be identified for each programme. The number of partnerships needs to be established, and respective roles need to be decided. Clear allocation of budget and resources needs to be identified. The event calendar and the responsible agencies for each programme need to be established.

b) Implementation

During the implementation of each respective programme, an evaluation of the impact of the programme needs to be collected and recorded. Clear measurement metrics for the impact need to be decided. Some metrics include a) Awareness of financial literacy b) Awareness of digital literacy c) Engagement during the programme d) Fraud literacy e) Digital payment literacy

c) Outcome

Reports on the number of individuals trained in the literacy programme or the number of participants in the awareness programme, and follow-up data collection on the increase in sales of the merchants who participated in awareness or training programmes.

d) Reports

Reports that contain key indicators from each stage need to be submitted by the responsible agencies. This reporting should be submitted every quarter, inclusive of challenges faced and interventions to be implemented in upcoming programmes.

As for research objective 3, small group interviews can be done during the event to acquire rich and in-depth data on the barriers to adopting digital payment, especially among merchants and the elderly group. Future research should include a more comprehensive measurement of digital financial literacy. This measurement consists of dimensions such as:

Basic knowledge and skills;

Awareness (knowing about available financial and digital products and services);

Practical know-how (knowing how to practically access and use digital products and services);

Decision making (including financial attitudes and behaviours); and

Self-protection (including consumer protection and data privacy) (Lyons, 2021).

For research objective 4, we proposed two Ecosystem-based Awareness Programmes that can complement the current cashless programmes. We propose the creation of 1) an Ecosystem-based Awareness Programme for micro, small, and medium enterprises (MSMEs) that aims to build a robust ecosystem for the adoption of cashless payment systems and 2) an Ecosystem-based Awareness programme for Cashless Use among the Elderly. The first programme focuses on educating micro, small, and medium enterprises (MSMEs) about the benefits of cashless payments while fostering collaboration among key stakeholders, including government agencies, financial institutions, and digital service providers. Key components of the ecosystem involve leveraging the unique roles of each stakeholder. An awareness programme can involve the relevant stakeholders that are integral to the business management, which includes:

Business Registration,

Licensing Training & Capacity Building,

Tax management,

Employee Fund,

Incentives, Loans & Grants and

Security.

Another possible Ecosystem-based Awareness Programme can target the elderly group and promote financial inclusion in the cashless payment landscape. This programme is designed to educate elderly individuals about the benefits of cashless payments while promoting collaboration among key stakeholders, such as government agencies, financial institutions, and digital service providers. The awareness programme can cover related activities in the elderly ecosystem, such as:

Banking and Investment Management,

Pensions,

Financial Assistance Programmes,

Healthcare Subsidies,

Digital Literacy, and

Cybersecurity and Digital Safety

Conclusion

The study evaluated the Cashless Society Programme (CSP) organised by MCMC and its partners, finding that it positively influenced society, with over 50 per cent of respondents expressing an intention to continue using cashless payments. Many participants appreciated the efficiency and security features of cashless payments, and the programme increased awareness of transaction safety. However, the study highlighted the need to address barriers faced by elderly individuals, such as computer anxiety, lack of technical skills, and concerns about security, which hinder their adoption of cashless systems. The research also noted a lack of sufficient data on merchants' adoption of cashless payments and recommended further studies to address these issues. A more inclusive approach to cashless adoption, including nationwide evaluations, would help overcome these challenges.

Additionally, the study assessed how CSP aligns with national strategies like MyDIGITAL and Ekonomi MADANI, showing that it supports digital inclusion, financial literacy, and MSME development. However, gaps such as limited outreach and evaluation mechanisms were identified. The research proposed an evaluation framework to guide the planning and implementation of cashless initiatives, recommending the development of key performance indicators (KPIs) by relevant agencies. The study also emphasised the importance of improving digital literacy to bridge the digital divide, particularly regarding mobile device usage and digital payments. Finally, the research suggested complementary initiatives to raise awareness about cashless payments, focusing on underserved groups like MSMEs and the elderly, to further enhance the inclusivity and security of Malaysia's cashless ecosystem. The study proposed complementary programmes such as Ecosystem-based Awareness for MSMEs and the elderly. For instance, agencies could collaborate to raise awareness about how cashless payments facilitate business processes like registration, licensing, loan applications, taxation, and cybersecurity. These initiatives would help address the digital divide and promote inclusivity in cashless adoption.

References

Anderson, L. W., Krathwohl, D. R., Airasian, P. W., Cruikshank, K. A., Mayer, R. E., Pintrich, P. R., Raths, J., & Wittrock, M. C. (2001).

A Taxonomy for Learning, Teaching, and Assessing: A Revision of Bloom's Taxonomy of Educational Objectives. New York: Longman.

Astro Awani. (2022, October 29).

BNM launches e-Duit campaign, focusing on e-payment education. Astro Awani. https://international.astroawani.com/malaysia-news/bnm-launches-eduit-campaign-focus-epayment-education-388416

Bank Negara Malaysia (2022).

Financial sector blueprint 2022-2026. https://www.bnm.gov.my/publications/fsb3

Bank Negara Malaysia (2022, October 29).

BNM further advancing e-payment adoption and financial inclusion. https://www.bnm.gov.my/-/e-duit-itekad-launch

Bank Negara Malaysia. (2022).

Promoting safe and efficient payment and remittance services. https://www.bnm.gov.my/documents/20124/10150308/ar2022_en_ch1e.pdf

Bernama. (2021, March 21).

Melaka launches Melaka Pay mobile apps. Bernama.com. https://bernama.com/en/news.php?id=1944408

Bernama. (2022, August 27).

ReDI to help expand digitalisation agenda to rural areas – PM. Bernama.com. https://bernama.com/en/news.php?id=2115004

Bernama. (2024, April 01).

BSN, PayHunter facilitate 24 ramadan bazaar spots in Kuala Lumpur to go cashless. Bernama.com. https://www.bernama.com/en/ news.php?id=2282239

The Star. (2022, August 25).

Digital banking solutions to serve remote communities. The Star. https://www.thestar.com.my/metro/metro-news/2022/08/25/digital-banking-solutions-to-serve-remote-communities.

Digital News Asia. (2022, July 18).

Touch 'n Go eWallet, PayNet launch 'mai kita cashless campaign at farmer's market in Kedah. Digital News Asia. https://www.digitalnewsasia.com/digital-economy/touch-n-go-ewallet-paynet-launchmai-kita-cashless-campaign-farmers-market-kedah

Digital News Asia. (2024, January 22).

TNG digital, PayNet unite to propel sabah toward a cashless society. Digital News Asia. https://www.digitalnewsasia.com/business/tng-digital-PayNet-unite-propel-sabah-toward-cashless-society.

Ekonomi Madani. (2023).

Ekonomi Madani: memperkasa rakyat. https://www.pmo.gov.my/ms/membangun-malaysia-madani-2/ekonomi-madani-memperkasa-rakyat/

EPU. (2021).

Pelan strategik unit perancangan ekonomi jabatan perdana Menteri 2021-2025. https://ekonomi.gov.my/sites/default/files/2022-01/Pelan%20Strategik%20EPU%202021-2025.pdf

Mahadi, N. (2021).

Understanding the barriers to cashless adoption among elderly Malaysians. ProQuest Dissertations Publishing. https://www.proquest.com/openview/ 6fd0b56d3551b51cdb08b160e83ef3b8/1

Kedah PBT. (2023, February 13).

Majlis pelancaran program e-duit desa di Jeniang. https://pbt.kedah.gov.my/index.php/2023/02/13/majlis-pelancaran-program-e-duit-desa/#:~:text=Telah%20berlangsungnya%20Pelancaran%20 Program%20E,elektronik%20(e%2Dpembayaran).

Malay Mail. (2023, November 09).

Sabah launches state-owned financial superapp YONO. Malay Mail. https://www.malaymail.com/news/malaysia/2023/11/09/sabah-launches-state-owned-financial-superapp-yono/101168

Malay Mail. (2024, July 23).

In a pilot project with U Mobile, four KL public schools to use cashless payments. Malay Mail. https://www.malaymail.com/news/malaysia/2024/07/23/in-a-pilot-project-with-u-mobile-four-kl-publicschools-to-use-cashless-payments/144709

Malay Mail. (2024, September 26).

Cashless payment system drives rural growth, foster economic resilience among Felda settlers in Pahang. Malay Mail. https://www. Malaymail.com/news/money/2024/09/26/cashless-payment-systemsdrive-rural-growth-foster-economic-resilience-among-felda-settlers-in-pahang/151673

Malaysia Kini. (2019, May 26).

Konsep bayaran tanpa tunai di bazar ramadan Kg Baru disambut baik. Malaysia Kini. https://www.malaysiakini.com/news/477425

Malaysia Reserve. (2024, May 29).

PayNet's bold move towards a cashless feature in education. The Malaysia Reserve. https://themalaysianreserve.com/2024/05/29/paynets-bold-move-towards-a-cashless-future-in-education/

MDEC. (2024).

Meningkatkan daya saing digitalisasi melalui jelajah saya digital. https://mdec.my/media-release/news-press-release/324/MENINGKATKAN-DAYA-SAING-DIGITALISASI-MELALUI-JELAJAH-SAYA-DIGITAL

Pahang Digital Plan. (2021).

Pelan digital Pahang. https://www.pahangdigital.com/ content.html Pahang Go (2024). PahangGo. https://pahanggo.com/

PayNet. (2024).

PayNet empowers pasar malam belia N6 Metrocity to spearhead Sarawak's largest cashless market. PayNet. https://paynet.my/press-release/2024/PayNet-Empowers-Pasar-Malam-Belia-N6-MetrocityTo-Spearhead-Sarawaks-Largest-Cashless-Market.pdf

Statisca.com. (2024).

Recent e-wallet usage in Malaysia 2023 by brand. https://www.statista.com/statistics/1460205/malaysia-recent-e-wallets-used-by-brand/

Suara Sarawak. (2024, March 21).

Bazar Ramadan tanpa tunai perlu diteruskan. Suara Rakyat. https://suarasarawak.my/bazar-ramadan-tanpa-tunai-perlu-diteruskan/

Teoh, K. Y., Tan, S. W., & Yusof, A. R. (2022).

Understanding the cybersecurity challenges for elderly users in a digital economy. Cybersecurity and Digital Economy Journal, 11(2), 67-89.

Malaysian Communications and Multimedia Commission

MCMC HQ Tower 1, Jalan Impact, Cyber 6,

63000 Cyberjaya Selangor Darul Ehsan, Malaysia

T: +603 8688 8000 | F: +603 8688 1000 | W: www.mcmc.gov.my